Britain For Sale - is nothing sacred

With so many businesses having been sold to overseas buyers, Alistair Schofield considers the question as to whether this is a good thing or not. It all started in 1962 when London Bridge was sold to the American Robert McCulloch for $2.46m and shipped to Lake Havasu in Arizona. On that day, the British posted the ‘For Sale’ sign on everything from companies to antiques. Since then we have privatised and sold state assets such as electricity companies, water utilities utilities, British Coal, British Telecom, British Steel and even the MOD's defence research laboratories. As a result, much of our water is now supplied by French companies, British Steel is now part owned by the Dutch following its merger with Koninklijke Hoogovens to form Corus, part of British Telecom has been sold to the Spanish and many of our electricity companies have been sold to French and American companies. This trend has not been unique to the public sector. In the private sector, ICL was sold to the Japanese, Rolls Royce and Bentley to the Germans, Abbey National to the Spanish and, with the notable exceptions of Michael Hestletine’s objections to the sale of Westland Helicopters in 1986 and the current debate surrounding the potential sale of the London Stock Exchange, there appear to have been hardly any objections. |

In contrast, it seems that most other nationalities are willing to fight ferociously to retain possession of what they perceive as their national assets – consider the reaction of the Germans when Vodafone launched their hostile bid for Mannesmann in 1999. Objections rained in from employees, the trade unions and every major political party. The same is occurring today in France over Mittal Steel’s bid for the steel company Arcelor where the French Finance Minister Thierry Breton has personally involved himself in the negotiations to, as he put it, ”defend the national interest”. Even in the United States, long-since considered the global leaders of free-market capitalism, Congress is attempting to block the sale of UK shipping and ports group P&O to Dubai Ports World on the grounds of national security.

Leaving aside the more emotive subject of national pride, the question is whether the British should be so relaxed regarding the ownership of companies or whether a more protectionist approach would be beneficial?

Protectionist approach

In the past the ownership of some businesses was regarded as a strategic necessity on grounds of national security, e.g. coal for power, steel for use in ship building, agriculture for food etc. However, in today’s environment, national economies are so integrated and interdependent that this objective is arguably unachievable, even if it is desirable. Take food production as an example; whereas this was once an entirely domestic industry, today a crop grown in one country will be harvested by migrant workers from another, flown to another for processing and packaging before finding itself on supermarket shelves in several other countries. According to research carried out by Sustain in 2001, the ingredients contained in a traditional Christmas dinner could have traveled a total of 24,000 miles before arriving on your plate.

However, possibly it is because of the globalisation of labour markets that the ownership of companies is so important? If it is more cost-effective to use manufacturing or processing services abroad, then we will not be creating jobs in the UK. But if the businesses are owned by UK residents, at least the profits will return here to be spent on British services and in British shops.

Free market approach

The buying and selling of British companies is nothing new, as a look back at the list of companies listed on the London Stock Exchange will reveal. If you compare the FTSE 100 of today with the list of 1984 when the index was first created, only about 40% of the original names remain.

Arguably this process of growth, decline, merger and acquisition is a natural and healthy feature in a vibrant economy; after all, the growth and sale of companies releases capital that can be invested in new business ventures and the fluctuating fortunes of businesses helps create new openings for others to exploit.

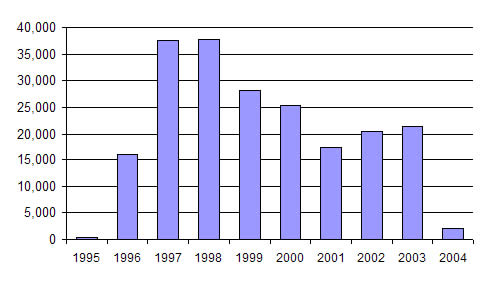

But is it the case that we are investing in new business ventures? As the following table demonstrates, the evidence suggests that we are. Although the numbers fluctuate year on year, during the 10 yeas from 1995 to 2004, on average there were 20,639 more new businesses registering for VAT each year than there were businesses deregistering.

Annual net registrations and de-registrations for VAT in the UK

|

Source: Small Business Service, DTI |

The conclusion I draw from this is that as long as we continue to reinvest in new businesses and we continue to innovate, then the ongoing process of selling off our more established and older businesses is not a problem. However, it makes the role of Government in supporting the small business sector all the more vital as, in the face of increased cost-competition from international markets, innovation is one of the few markets that we are still able to compete in.